Now that we’ve covered the basics of interest rates, let’s get to applying them—with discounting.

This isn’t the type of discounting you see at an outlet mall, with big signs screaming “EVERYTHING MUST GO!!!” This is the kind of discounting rich people are interested in. It’s a concept used when you want to figure out how rich you are going to be.

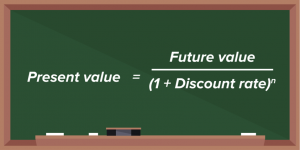

Let’s say you want to be a millionaire. The discounting formula will tell you how much you’ll need to start—and how long you’ll have to invest that money—to get there.

Pretty self-explanatory. Your future value is what you want in the future—in this case, $1,000,000. The discount rate is the interest rate—how much your investment will pay each year.

And n is the number of years you’ll need to stay invested.

We want to find out what we need to start with now, and that’s present value.

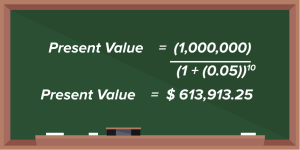

So if your savings account is paying 5% interest, and you want to become a millionaire in 10 years, here’s the amount you’ll need to start:

The discount rate is a pretty easy concept to grasp. And it’s also extremely important. It is something that governments, businesses and individual investors use in making accurate projections of future money.

It’s important to understand how these formulas work (and why they work), but the truth is, most of us are going to use calculators to crunch the numbers. And as it happens, we’ve got one right here!

Below is a Present Value calculator. To use it, plug in your Future Amount, interest rate (this calculator uses r, while others will use i), and number of periods (n). It’ll spit out your Present Value.

You want to have $5,000 in two years, and you’re investing your money in a savings account that pays 5% interest. How much do you need to invest today?

OK, in the previous step, we knew the amount of money we wanted in the future, and needed to figure out how much to invest today. Now let’s look at the reverse.

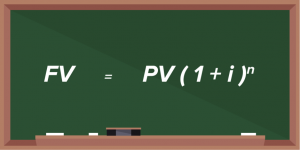

Let’s say you have some money to invest today, and you want to know how much it will be worth in the future. That’s called calculating Future Value.

If you don’t reinvest the interest you earn each year, your calculation is called future value using simple interest. As its name suggests, it’s a simple calculation—but it doesn’t really interest us, and here’s why:

Remember how in the previous step we needed to invest $613,913.25 at an interest rate of 5% to get to $1 million after 10 years? That translates into growth of 63%!!!!!!!!!!!!!

And the reason the original amount grew that much is because of compound interest. This is the process of earning interest not just on your principal, but also on the interest you earned in previous years.

Yeah—this is where interest gets…interesting.

Future Value at Compound Interest

Now the equation for future value using compound interest looks like this:

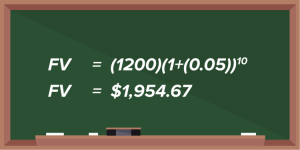

Let’s say you don’t have over $600K to invest. Instead, you’ve got a more realistic $1,200. And again, your interest rate is 5%, and you’re going to stay in for 10 years. Just look at the effect of compounding interest:

Yup. Just as it did in the Present Value example, your money has grown 63%!!

As you can see, compound interest will help your money make more money pretty darn fast.

On and On and On and…

Here at WSS, we’re the first to admit that math can be pretty dry at times. So let’s take a little break by engaging in some dreams. You know those lotteries that’ll pay you $1,000,000 every year for the rest of your life? We’re running one of them for all WSS members, RIGHT NOW!!

That’s right, if you complete this course, you’ll be entered into a lottery where you could win $1,000,000 a year for life. The earlier you finish, the better your chances, so get going and finish this course.

Nah. Come on, do you really think we have that kind of cash to throw around? Like we said, just engaging in a dream. But that dream is actually kind of useful, because the kind of lottery prize we just described is something called an annuity—an instrument that pays out money in regular installments every year.

And there’s a really interesting kind of annuity that pays out those installments FOREVER. It’s called a perpetuity.

Perpetuities

The word perpetuity comes from the word perpetual, meaning that it never stops.

One popular example is an investment called the British consol. The consol is a bond that can be bought from the British government that entitles the bondholder to interest payments forever.

Calculating the Present Value of a Perpetuity

Now the first question anyone will have about this kind of investment is, “How much is it worth?”

And the answer might seem impossible. After all, how could you ever calculate the present value of an investment that will earn interest forever?

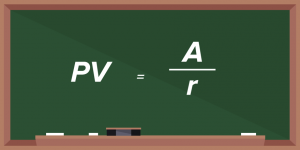

We don’t quite know how they did this, but apparently some mathematicians figured it out. And here’s the equation they came up with:

The term A represents the amount received per year, and r represents the rate of return, or interest rate. PV, as we already know, is the present value.

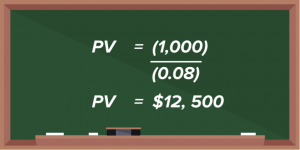

Let’s look at an example: say we have a perpetual annuity that pays $1,000 per year at a rate of 8%. The present value of that annuity would be...

This perpetuity is worth $12,500.

Now this might seem like a really low number. But it makes more sense when you realize that a perpetuity is different from a bond. With a bond, you pay a principal amount, you get interest on that principal over the life of the bond—and at the end you get the principal amount back.

A perpetuity is the same, with one exception—you never get the principal amount back. And that exception is really important, because if you’re only getting the interest payment back, you’re giving up a lot of income now for a stream of income that declines in value in the future. Think about it. What is the value of $1,000 paid 500 years from now? A thousand years from now? A million years from now? Essentially nothing.

Fortunately, those same math whizzes who figured out the value of a perpetuity also designed a perpetual annuity calculator for us. Try this on for size:

You have a perpetual annuity that pays out payments (d or A) of $500 per year at a discount rate (r) of 10% and has a growth rate of 0. The present value of that annuity would be...

If you got $5000, then you got it right!

Worth Your Time

So what does all this have to do with investing?

Good question. The concepts we’ve studied so far are very useful when it comes to retirement savings, and you need to know about them to become a real investment pro. Preparing for retirement involves setting up the right kind of annuities, so that you have a reliable cash flow and don’t end up eating cat food in your old age.

And there’s more. Time has a huge effect on the performance of bonds, company stocks, and real estate. You need these concepts to figure out not just what your investments are worth now, but what they will be worth in the future.

Next up we’re going to take a look at something called the Discounted Cash Flow model. You’ll be able to impress your friends and family by telling them what it is, which alone is worth your time. But it will also help you do your own valuations of things like stocks and bonds. And in investing, that’s where the action is.