Have you ever thought about how your household wealth or annual income stack up to others your age, or how others made their first million dollars?

It’s natural to want to compare nest eggs and to wonder how much the wealthiest of the wealthiest in our age groups earn, right? Well, we’ve got the answers!

We’re going to talk about how much money you need to earn in order to be in the top 1% for your age.

Net Worth Defined

Let’s start by talking about what net worth really means.

You might think that your net worth is defined by how much money is in your bank account, how much money your house and car are worth, or how much money you have invested in stocks.

All of these are partially right, but they leave out one annoying (but important) detail: debt.

To calculate your net worth, use the following equation:

Net Worth = Total Assets – Total Debt

Unfortunately, your debt can seriously change your net worth.

For example, you might own a house that’s worth $300,000. But if you still owe the bank $250,000 on your mortgage, you have to subtract that number out, which means that’s only $50,000 going towards your net worth.

When you calculate your total assets, take into account the total value of everything you own.

That means checking accounts, savings accounts, investments, real estate, cars, cash, jewelry, and even household items that still hold any value.

When calculating debt, think about student loans, car loans, mortgages, personal loans, credit card debt and any other money you owe the bank, a business, or another person.

Now, before we talk about how high your net worth has to be for you to be in the top 1% of your age group, let’s talk about HOW these top one-percenters got there...and what you can do to increase your net worth as well!

Survey of Millionaires

Personal Finance guru Dave Ramsey released a study of 10,000 millionaires in April, 2023 and he found:

- Most use a written grocery list when shopping.

- 8 of 10 millionaires invested in their company’s 401k retirement plan.

- The top careers were engineer, accountant, teacher, management and attorney.

- 79% received NO inheritance.

- 75% said “regular and consistent investing over a long period of time leads to success.”

Based on that research of millionaires, here are some of the most important tips that will help increase your net worth over time.

Make a Budget

Along the lines of using a grocery list, making a budget is step one for personal finance.

You won’t be able to build the retirement fund you want if you don’t know how much you’re earning, spending, and saving!

Ideally, you want to be saving at least 20% of your income and putting it towards retirement.

We highly recommend the 50/20/30 rule, which states that your essential expenses (rent, gas, insurance, etc.) should add up to no more than 50% of your household income. Then, you should put 20% towards savings (emergency fund, Roth IRA, 401(k), etc.), and the remaining 30% is for your personal use.

If you’ve taken a look at your earnings and spending habits and noticed that your expenses seem to be too high for your household income, it may be time to make some tough decisions.

Is your rent alone more than 50% of your household income? It might be time to downsize to a smaller living space and take on a roommate.

Are your personal expenses looking way out of proportion? It might be time to cancel some entertainment subscriptions, start making your morning coffee at home, or going out to eat less.

Do you have your expenses in check but they still seem to be too high for your household income? You might want to consider getting a second job or running a side hustle to pull in some extra cash.

Invest in a Retirement Account

Now that you’re saving 20% of your annual income, it’s time to do something useful with it!

If you have a job that offers a 401k–take it. If your employer matches some of your retirement savings, then max out on their match! If you don’t have a 401k then a Roth IRA is one of the most valuable tools a young investor can have in their tool belt.

The magic of the Roth IRA happens due to the fact that you’re allowed to make your contributions with after-tax dollars.

You make your contributions without the tax deduction you get when you contribute to a traditional IRA, and then your money is allowed to grow completely tax-free.

WEALTH BUILDING TIP: If your company doesn’t offer any retirement accounts, then see our Robinhood IRA Review, start your own retirement account, and get some matching funds (ie, see what their current match % is to see how much free money you will get).

That’s right; you pay absolutely no taxes on the money in your Roth IRA when you withdraw it in retirement.

The Roth IRA makes perfect sense for young individuals who plan on being in a higher tax bracket in retirement than the one they’re in now.

That way, you can pay your taxes now while your tax bracket is still lower and not have to worry about it when you retire!

It’s very important that you open your Roth IRA as soon as possible; you can only contribute $6000 a year to it and there are also restrictions that prevent you from contributing once your annual income reaches a certain level.

To learn about our #1 recommended Roth IRA provider, read our Robinhood IRA review!

Invest in Index Funds

Now that you’ve got yourself investing in your 401-k or a Roth IRA, it’s time to decide what exactly you want to invest in!

If you don’t have the time, experience, or interest necessary to pick individual investments for yourself, we recommend starting by investing in index funds.

Index funds are the cheaper, quicker, and more easily accessible cousin of the typical mutual fund.

Instead of being expensive, actively-managed funds that you can only trade at certain times, index funds are managed passively and are often traded on the market like regular stocks in ETF form.

These funds are tied to a specific benchmark index and they aim to mimic or “track” this benchmark.

Index funds usually have very low fees compared to mutual funds.

You can find an index fund for just about any sector, security, or investment strategy you desire.

Do you have a strong interest in the tech industry? There’s an index fund for that.

Do you want to gain some exposure in the bond market? There’s an index fund for that.

Do you want to make a one-stop investment in a portfolio that is perfectly diversified into large-cap domestic equities, small-cap domestic equities, foreign investments, and bonds? You guessed it – there’s an index fund for that.

Buying an index fund ETF is a great way to achieve some diversification without buying tons of individual securities.

For example, if you invest in an index fund that tracks the S&P 500, you are mirroring the S&P 500 Index exactly. You are invested in all 500 companies on the index with the same weights as the actual S&P 500. That’s a lot of diversification just for buying one security!

If you do want to invest in an S&P 500 ETF, you can start with IVV (from iShares), SPY (from SPDR), or VOO (from Vanguard).

ALERT: You can access all three of these ETFs and many more, and get up to $1,700 in free stock when you open a ROBINHOOD account.

Then Buy Good Growth Stocks

So now that you have a good budget, are saving in a retirement account, and buying index funds, its time to buy some individual stocks so that your overall portfolio can outperform the market overall.

If you don’t want to be a hands-off investor and you want to put the time and effort into investing in individual stocks, you’ll need a little help deciding what to buy and what to pass on.

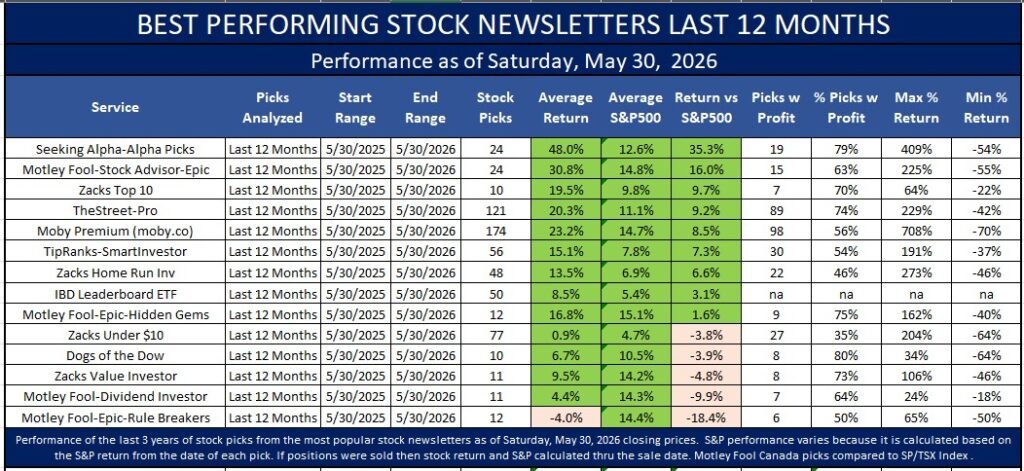

There are many very good stock picking newsletters out there that are priced at $100 or less that consistently beat the S&P500. Take a look at our ranking of the best stock newsletters of 2025. Table is based on May 31, 2025 data. For a full detail analysis, see our article on the best stock newsletters here.

So, to help you get started with buying individual stocks, here are 3 services that are time tested and consistently beat the S&P500:

The Motley Fool has been crazy consistent with their stock picks, with their Stock Advisor list outperforming the S&P 500 by over 5x since it was started in 2002.Their system is simple: twice a month they come out with their latest pick; and twice a month you get a list of their 5 Best Stocks to Buy Now. With over 500,000 subscribers, they must be doing something right. Read our Motley Fool Review to see if is worth it or go straight to the Motley Fool promo page to see their best current offer.

If you live outside the United States, then you unfortunately won’t be able to open an account with many U.S.-based brokerages. There is one global broker we like if you want to open an investment account and invest in ETFs and other securities on 135 exchanges across 33 countries, check out Interactive Brokers.

Interactive Brokers is our #1 recommended brokerage for international traders, and they’ve been recommended by plenty of other platforms as well.

Get a Credit Card

If you’re comfortable with the way you’ve been budgeting and saving, then it might be time to take on the responsibility of having a credit card.

Credit cards can be a great way to spend money securely while building credit, but credit card debt can be EXTREMELY dangerous if you let it get out of hand.

With insanely high interest rates and late fees, there is no reason you should ever carry a balance on a credit card unless it’s absolutely necessary.

You should view a credit card as a simple personal finance tool that you’ll use to help you build credit, not as a way to spend money you don’t have now and pay it back later.

When it comes to building your credit with your credit card, there are two important things you’ll want to pay attention to.

Firstly and most importantly, always pay your credit card balance off in full, every month, every time.

This is one of the most important factors that affects your credit score.

Your credit score will take a hit if you make even one late payment.

Secondly, pay attention to how much of your line of credit you’re using.

Ideally, credit rating agencies like to see you using no more than 30% of your available credit every month.

So, if you have a credit card with a $1000 limit, use it to spend $300 or less every month, and then be sure to pay it off in full.

If you’re not sure where to start or you’re overwhelmed by the seemingly infinite amount of credit cards out there, you can use Credit Karma to help you make a decision.

Credit Karma will tell you your credit score (without using up your official credit report request), recommend credit cards for you based on your credit score, and even give you tips on how to improve your credit!

Top 1% Net Worth By Age

Be honest with me here: did you skip the middle of this article and scroll right down here to find out the juicy details?

If so, good for you; you were on a hunt for some information and you found it!

But simply knowing how much other people are worth won’t do you any good.

It’s important to know HOW to build wealth and achieve your financial goals, and that’s the kind of information we included above. Be sure to scroll up and learn how to start increasing your net worth!

Without further ado, it’s time to talk about how much your net worth needs to be for you to be in the top 1% for your age group!

Let’s start with an average net worth.

According to The College Investor, the average net worth of a 22 year old is…

…-$39,915.

That’s right, NEGATIVE. How is this possible?

Well, many 22 year olds come out of college with massive student debt.

On top of that, if they decide to buy a car or a house via a loan, then the “debt” part of their household net worth will go up even more. There’s also income inequality that can affect an individual’s net worth.

As you can see, debt can put a huge damper on your net worth.

But there is hope; as you start paying off your debt (thus gaining equity in your assets) and putting more money into your savings and retirement accounts, you’ll see your net worth climb!

Here are the rest of the stats:

- Average net worth of a 25 year old: -$23,704

- Average net worth of a 30 year old: -$1,043

- Average net worth of a 35 year old: $25,517

- Average net worth of a 39 year old: $69,761

Those statistics were just averages. Now, let’s get into the fun stuff! Here is the top 1% net worth by age group, courtesy of DQYDJ:

- Top 1% net worth for ages 18-24: $435,076.59

- Top 1% net worth for ages 25-29: $606,188.36

- Top 1% net worth for ages 30-34: $956,944.74

- Top 1% net worth for ages 35-39: $4,034,486.45

- Top 1% net worth for ages 40-44: $7,909,636.79

- Top 1% net worth for ages 45-49: $10,494,100.10

Sounds easy enough, right?

Just kidding; these household net worth levels are insanely high for these ages and a vast majority of people do not reach these net worths. But don’t lose hope!

While the wealth gap between younger people and older people might seem enormous, don’t forget about the power of compound interest. If you keep saving money and investing, your returns will keep building at an exponential rate!

Average Income By Age

According to DQYDJ, the average incomes every year by age is as follows:

- Average income of a 25 year old: $41,461

- Average income of a 35 year old: $66,320

- Average income of a 45 year old: $79,101

- Average income of a 55 year old: $77,308

Top 1% Income By Age

According to Financial Samurai, the top 1% annual income by age group is:

- Top 1% income for ages 27-31: $170,000

- Top 1% income for ages 32-36: $210,000

- Top 1% income for ages 37-41: $260,000

- Top 1% income for ages 42-46: $320,000

Do these average income and top 1% income numbers surprise you? Let us know in the comments below!

Final Thoughts

While it might not be realistic to expect to be worth $400,000 by the time you’re 24 or a million dollars by the time you’re 30, you can follow the steps we talked about earlier in the article to make sure you can have the retirement you want.

Well, there you have it – we know that there are some crazy high earners out there and while your net worth might not be in the top 1% for your age right now, you certainly do have access to the tools that will help you get there down the road!

Rank of Top Stock Newsletters Last 3 Years, as of May 31, 2026

We are paid subscribers to dozens of stock and option newsletters. We actively track every recommendation from all of these services, calculate performance, and share our results of the top performing stock newsletters whose subscriptions fees are under $500. The main metric to look for is "Return vs S&P500" which is their return above that of the S&P500. So, based on May 31, 2026 prices:

Best Stock Newsletters Last 3 Years' Performance

| Rank | Stock Newsletter | Picks Return | Return vs S&P500 | Picks w Profit | Max % Return | Current Promotion |

|---|---|---|---|---|---|---|

| 1. | Alpha Picks | +110% | +83% | 76% | 1,571% | June, 2026 Promotion: See all their picks & get $124 off |

| Summary: 2 picks per month based on Seeking Alpha's Quant Rating; consistently beating the market every year since launch; tells you when to sell and they have sold almost half. See complete details in our Alpha Picks Review. Or get their Premium service to get their QUANT RATINGS on your stocks to better manage your current portfolio--read our Is Seeking Alpha Worth It? article to learn more about their Quant Ratings. | ||||||

| 2. |  Zacks Value Investor | +58% | +46% | 53% | 1,134% | June, 2026 Promotion: $1, then $495/yr |

| Summary: 10 stock picks per year on January 1st based on Zacks' Quant Rating; Retail Price is $495/yr and includes 6 different services including those below. Read our Zacks Review. | ||||||

| 3. | Zacks Top 10 | +31% | +19% | 74% | 170% | June, 2026 Promotion: $1, then $495/yr |

| Summary: 10 stock picks per year on January 1st based on Zacks' Quant Rating; Retail Price is $495/yr and includes 6 different services. Read our Zacks Review. | ||||||

| 4. |  Action Alerts Plus | +20% | +6% | 61% | 208% | Current Promotion: None |

| Summary: 100-150 trades per year, lots of buying and selling and short-term trades. Read our Jim Cramer Review. | ||||||

| 5. |  TipRanks SmartInvestor | +13% | +5% | 57% | 266% | Current Promotion: Save $180 |

| Summary: About 1 pick/week focusing on short term trades; Lifetime average return of 355% vs S&P500's 149% since 2015. Retail Price is $379/yr. Read our TipRanks Review. | ||||||

| 6. | Zacks Home Run Investor | +7% | +2% | 43% | 337% | June, 2026 Promotion: $1, then $495/yr |

| Summary: 40-50 stock picks per year based on Zacks' Quant Rating; Retail Price is $495/yr. Read our Zacks Review. | ||||||

| 7. |  Moby.co | +19% | 0% | 55% | 797% | June, 2026 Promotion: Get #1 Stock Pick Free |

| Summary: All it requires is an email address to get their #1 stock pick free; 60+ stock picks per year, segmented by industry; consistently beating the market every year; retail price is $365/yr but save try it for $99. Read our Moby Review. | ||||||

| 8. | IBD Leaderboard ETF | 11% | -1.8% | n/a | n/a | June, 2026 Promotion: NONE |

| Summary: Maintains top 50 stocks to invest in based on IBD algorithm; Retail Price is $495/yr. Read our Investors Business Daily Review. | ||||||

| 9. | Zacks Under $10 | +0.4% | -3% | 33% | 263% | June, 2026 Promotion: $1, then $495/yr |

| Summary: 40-50 stock picks per year based on Zacks' Quant Rating; Retail Price is $495/yr. Read our Zacks Review. | ||||||

| 10. | Dogs of the Dow Strategy | +6% | --7% | 50% | 34% | Current Promotion: None |

| Summary: Buy the 10 highest yielding dividends stocks in the Dow Jones Industrial Average on January 1st and sell on Dec 31st each year. | ||||||

| 11. | Stock Advisor | +7% | -17% | 59% | 141% | June, 2026 Promotion: Get $100 Off |

| Summary: 2 picks/month and 2 Best Buy Stocks lists focusing on high growth potential stocks over 5 years; Retail Price is $199/yr. Read our Motley Fool Review. | ||||||

| 12. | Rule Breakers | +11% | -18% | 51% | 208% | Current Promotion: Save $200 |

| Summary: Rule Breakers is included with the Fool's Epic Service. Get 5 picks/month focusing on disruptive technology and business models; Lifetime average return of 355% vs S&P500's 149% since 2005; Now part of Motley Fool Epic. Read our Motley Fool Epic Review. | ||||||

| Top Ranking Stock Newsletters based on their last 3 years of stock picks covering 2026, 2025, 2024, and 2023 performance as compared to S&P500. S&P500's return is based on average return of S&P500 from date each stock pick is released. NOTE: To get these results you must buy equal dollar amounts of each pick on the date the stock pick is released. Investor Business Daily Top 50 based on performance of FFTY ETF. Performance as of April 5, 2026. | ||||||