Stocks aren’t just blips on a screen. They represent actual businesses, and you don’t know what you’re investing in until you learn how to value a business.

The Recipe to Value a Business

Here at Wall Street Survivor we like metaphors. We also like cake. So it shouldn’t come as a surprise that when you combine the two, we’re in heaven. So here’s our ultimate metaphor of awesomeness: a portfolio is like a cake.

OK, first of all, a portfolio is like a cake because it’s rich (get it?) and moist (um…sort of?) and just looking at it makes your mouth water (OK, let’s get back on track).

It’s also like a cake because you have to put the ingredients together according to the right recipe. (That would be your asset allocation). That recipe needs to fit in with your specific tastes (That would be your risk tolerance). And finally, it’s even more like a cake because if those ingredients—individual stocks—aren’t of good quality, the whole thing could leave a bad taste in your mouth.

If you’ve ever watched one of those reality TV cooking shows you’ll know that the key to success in the kitchen is choosing the right ingredients. (Seriously, who makes a cake with margarine instead of butter?)

In this course, we’re going to teach you about how to pick those ingredients. We’ll teach you how to find value in a company, how to size up its financial statements, and where to find the numbers that tell you about its future.

At the end, you’ll be just like an expert chef, sniffing out the difference between the good ingredients and those that are past their expiry date. And with that experience under your belt, it’ll be time for you to whip up your dream portfolio: one that’ll make your mouth water.

There’s a Value Behind That Business?

When you buy a stock, you’re literally buying part of a company. And to know if you’re buying at the right price, you have to know what its true value is.

Sophisticated investors do this by examining a company’s fundamentals. These are the basics of a company’s performance: how much money it’s earning, how much debt it has—the things that tell you what the value of a business is.

Fundamental Analysis—the basics of value for a business

You’ll hear the term “fundamental analysis” a lot in investing. But don’t get spooked by it. It’s just a fancy term for “doing your homework” when it comes to stocks.

That means analyzing all the things that affect the value of a business and its’ stock, instead of just relying on “hot tips” from the Internet or your neighbor. The problem with this is that there are an awful lot of things that affect the value of a stock.

First there are the obvious ones: things like sales, profit, how many assets the company has. General Motors for example, has an enormous amount of assets: all its factories and assembly plants add up to a whole lot of value. But remember that not too long ago, General Motors declared bankruptcy. And that’s because sales and profits were falling.

Then there are the intangibles: things like a company’s reputation, its brand recognition (Hello Coca Cola!) and the quality of its management. And finally there are the things that are beyond a company’s control—like the future state of the world economy, or the invasion of shape-shifting lizards from the Andromeda Galaxy. Clearly, this can get pretty complicated pretty quickly.

Let’s not get technical…

Now some analysts just throw up their hands at this point and decide not to bother. They either quit the business or do something called “technical analysis”. (We won’t get into that here, but it’s basically a way tp value a business based on market data and charts.)

But the rest soldier on. They recognize that there will always be uncertainty in the world but it’s also manageable. And part of managing it is just doing your homework – specifically by looking for stocks that cost less than their intrinsic value.

Finding the True Value of a Business

So what is intrinsic value of a business?

It’s an idea developed by someone named Benjamin Graham, who is also known as the father of value investing. (He actually taught Warren Buffett, so maybe he should be called the grandfather of value investing.)

Simply put, the intrinsic value of a business is its true worth—regardless of what the market says it’s worth.

You can see right away from that definition that Benjamin Graham didn’t believe that the market always gets it right. Sometimes it overvalues a company. Sometimes it undervalues it. After all, in the early 1980s, computer giant IBM hired a tiny, unknown company called Microsoft to develop software for the personal computers it was making. What IBM—and the market—didn’t realize, was what only Bill Gates and a few others did: the software would become more valuable than the machines that ran it. In 1996, Microsoft edged past IBM in market value. And Bill Gates became the richest man on the planet.

The point? If you buy an undervalued company, you’re set to make a profit.

“Attention Shoppers: Bargains on Tech Stocks in Aisle One…”

Ah, but if only finding an undervalued company was that easy. Unfortunately, the market doesn’t tell you when a company is on sale for a great price, the way that friendly grocery store voice does. You have to do the work to value a business yourself.

The way to do so is by asking some basic questions about a company. For example, is it turning a profit? Does it turn a profit all the time, or just every now and then? Does it pay a dividend? How is it doing compared to other companies in its sector? How about to the market as a whole?

As you can see, there are a lot of questions. And they only scratch the surface of the questions you need to ask.

Fortunately, however, the answers are readily available. They’re found in something called a company’s Financial Statements. Just like how you want to know what kind of ingredients are going to go into your cake, you want to know what kind of company you’re putting into your portfolio mix. At the grocery store, you read the label; in the stock market, you read the financial statements.

Using Financial Statements to Value a Business

Any company that is publicly traded has to release financial statements—it’s the law. There are quarterly financial statements and annual ones. They’re very easy to find, since almost all big companies have them on their website.

Financial statements present a snapshot of a company’s financial health. They show how well a company is running its business, so that shareholders can decide on its management’s performance and so that other investors can decide whether to become shareholders themselves.

The Basics of Financial Statements

There are a number of different kinds of statements, depending on the business a company is in, but in general they’ll include the following as their core:

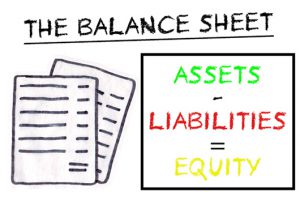

This statement tells you a company’s financial position at a given date: what the company owns and what it owes.

What it owns is known as its Assets: things like cash, factories, land, and inventory.

What it owes is its Liabilities. Those are things like bills it still has to pay or money it has borrowed from the bank.

Now once those bills are paid, what happens to the value that’s left? Well, it belongs to the owners of the company—naturally. That’s their share, and it’s called Shareholder Equity.

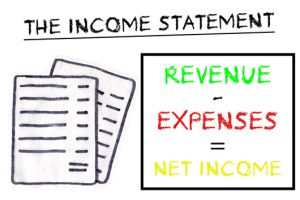

The income statement tells you how well the company’s business is doing. It shows Revenues, which is basically how much money the company earned from its sales. It also shows Expenses, which is how much money the company spent to run its business.

The difference between these two is called Net Income—and it tells you if the company made a profit or not.

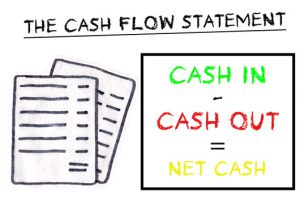

The cash flow statement shows how much cash was brought into the company (through things like sales, or taking out a loan from a bank) and how much went out the door (to employees, suppliers, the bank, and even the tax man). As they say, “Cash is King”. It’s important to know how much cash a company has readily available at any given time.

Making Money: Earnings

OK, so now that we’ve been introduced to Financial Statements, let’s recall what they’re for. Remember that while people may invest for a number of reasons, their single overriding goal is always the same: to make money. (Otherwise it’s called “charity”.)

One of the main ways an investor makes money from a stock is through dividends. These are regular payments that most (but not all) companies make to their shareholders. A company that pays regular, strong dividends is an attractive investment.

But where does the money for those dividends come from?

Good question. And now we get to the most-watched, most-analyzed single item in investing: earnings.

Earnings are the profit that a company makes. They are used to pay for dividends—as well as for a lot of other things, like research and development, buying other companies, and huge bonuses to corporate execs.

Earnings are important because, more than anything else, they tell you how well a company is doing.

So, How Is the Company Doing?

Now while earnings may be heavily scrutinized, on their own they don’t tell you that much. After all, if a company announces really big earnings, that might just be because it’s a really big company. What we really want to know is how much the company is earning relative to its size.

For that, we don’t look at just earnings. We look at earnings per share.

This neat little ratio is written as EPS, and it’s easy to calculate. Just take the earnings figure from the Income Statement, and divide it by the number of shares outstanding. Presto! You now have a number that tells you how much each share earned.

And the great thing is, you don’t even have to do that yourself. It’s the norm for companies to calculate that number and report it in their statements. (Think of it at as a free, value-added service to current and prospective shareholders.)

So I should just look for companies with a high EPS and buy them?

Not so simple. To return to our cake analogy, there are lots of bakers out there looking for the best ingredients for their cake. If you’ve heard about a terrific ingredient at your local farmer’s market, it’s likely that others have as well.

So if a company has a high EPS, everybody will know about it. And like you, they’ll want to buy it, which pushes the price up.

So the real question is quite different: is the price of the stock a good one relative to the earnings?

And that leads to another ratio that is possibly even more important: the price/earnings ratio, or P/E.

This will tell you if a stock is expensive relative to its earnings, or fairly cheap. And as any savvy master chef knows, it’s better to buy cheap than expensive.

OK, so that’s it then, right? Just look for a low P/E and buy, buy, buy!

Not to burst your bubble, but again it’s a bit more complicated than that. Yes, a high EPS is good, and a low P/E is good. But what if other companies have better ratios?

This is where comparison comes in. You’ll want to look at other companies in the same industry and see what their ratios are like too. After all, if a company has a low P/E ratio but every other company in the same industry also has a low P/E—well, maybe the whole industry is cheap for a reason!

Time to investigate further.

Making More Money: Growth

So companies with a good EPS ratio—especially relative to other companies in the same industry—look like a good buy. But remember, in investing—just as in baking—looks can be deceiving.

Whenever you read an ad for a mutual fund, you’ll stumble across a standard disclaimer that goes something like this: “Past performance is no guarantee of future results.”

And that’s as true for an individual stock as it is for a fund. Past earnings are no guarantee of future earnings—and as an investor, you’re only interested in future earnings. The big question then, is how much will future earnings grow?

What Does Everyone Else Think?

Other than fortune tellers and psychics, the only people who can really predict a company’s future earnings accurately are company insiders—and you shouldn’t be talking to them, because you could get into trouble for insider trading.

Nonetheless, people try. They look at a variety of things. Is the company’s market growing—and if so, by how much? Is the company already a dominant player? Can it make gains at the expense of rivals? Is there room for high-end goods in the market that can deliver big profit margins?

Figuring all this out is a challenge. And here’s where we come back to the P/E ratio: it actually reflects what most investors think the growth of the company will be.

Think about it for a second. If some investors think a company’s growth will falter, they’ll sell the stock, which will drive its price down. But if other investors think growth will surge, they’ll be willing to pay more for the company—and drive the price up. The price at any given time will reflect the best estimate of everyone in the market.

But of course, investors can be wrong. And that’s what Fundamental Analysis is all about. It involves you doing your own research, and making your own estimations about a company’s future growth. Because, like Warren Buffet, you could come across value that others have overlooked. And that will make you a very rich investor.

Coming to Conclusions

As you’ve probably gathered by now, judging a stock price is as much art as it is science. You have to accept that some things—like a company’s future growth, or the state of the world economy—are uncertain; and that means relying on past experience, best estimates and your instinct when evaluating them.

But it doesn’t mean giving up facts. There are tangible, easily calculated measures like EPS and P/E that give you guidance. If a P/E ratio is extremely high for example, that means the market thinks future earnings will be very good. After all, that’s why they’re willing to pay such a high price for the stock: so they can receive all that income down the road. Maybe the market is right.

But maybe people have just been swept up by some fad that is not going to pan out. (Remember the tech bubble? ) And the last thing you want is to get swept up in the hype.

Fundamental Analysis won’t let you predict the future with absolute certainty. But it will give you the facts that can help guide your instinct, which is at the heart of all-intelligent investing.