If you’re researching investment tools, you’ve probably encountered Morningstar’s name attached to those familiar star ratings. But is paying $249 per year for Morningstar Investor actually worth it—or can you get by with free alternatives? This morningstar investor review breaks down exactly who benefits from the subscription and who should save their money.

Quick Answer: Who Morningstar Is Worth It For (and Who Should Skip It)

Let’s cut to the chase. Morningstar Investor at $249/year is genuinely worth it for serious, long-term investors who actively research mutual funds and ETFs, maintain portfolios above $50,000, and are willing to spend time analyzing their holdings. For casual investors who buy a single index fund and forget about it, or day traders needing real-time technical charts, it’s probably not worth paying for.

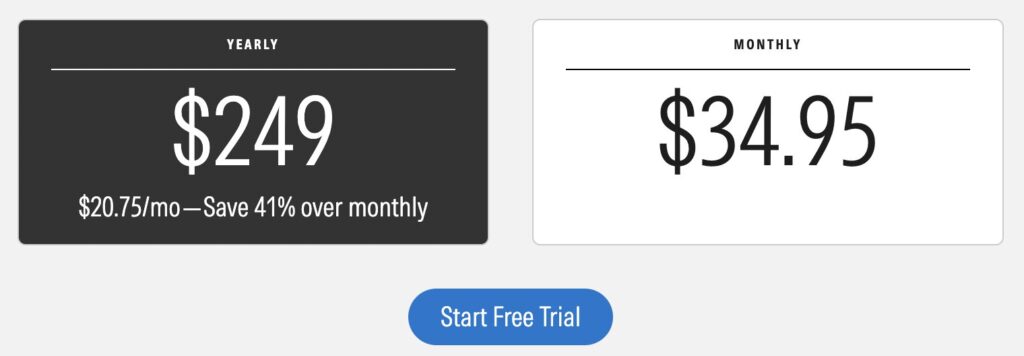

The current 2026 pricing sits at $249/year for the standard annual plan (roughly $20.75/month). New subscribers typically get a first-year discount around $199, and there’s a 7-day free trial to test the platform before committing. Monthly billing runs $34.95, so the annual option represents about 41% savings.

Here’s a quick breakdown of who benefits most:

- Long-term mutual fund and ETF investors: Often worth it. You’ll use the detailed analysis, Medalist Ratings, and Portfolio X-Ray tools to optimize holdings and reduce unnecessary fees.

- Data-driven DIY stock pickers: Likely worth it. Access to 120+ analyst reports on individual stocks and fair value estimates supports fundamental investors who read research before buying.

- Hands-off robo-advisor users: Probably not worth it. If algorithms manage your portfolio and you check it twice a year, you won’t extract enough value to justify the cost.

- Day traders and technical analysts: Not worth it. Morningstar focuses on long-term fundamentals, not real-time quotes or advanced technical charts.

The real value drivers are Morningstar’s proprietary ratings (which have over three decades of credibility since the company was founded in 1984), the depth of coverage on mutual funds and ETFs, and the Portfolio X-Ray tool that reveals hidden risks in your holdings.

Rule of thumb: If you log into your brokerage accounts less than once a month and don’t actively research your holdings, Morningstar Investor is probably not worth paying for.

What Is Morningstar & Morningstar Investor?

Morningstar is a Chicago-based independent investment research firm founded in 1984 by Joe Mansueto. What started as a newsletter providing mutual fund data has grown into a global powerhouse operating from over 40 offices worldwide, covering more than 600,000 securities and serving everyone from individual investors to institutional clients and asset managers.

The company splits into two main branches: its institutional business (serving financial advisors, retirement plan sponsors, asset managers, and banks) and its consumer product, Morningstar Investor. Launched in June 2022 to replace the older Morningstar Premium subscription, Morningstar Investor is the company’s single paid subscription for retail investors.

With Morningstar Investor, you get access to:

- Full analyst reports on stocks, mutual funds, and ETFs

- Star Ratings and forward-looking Medalist Ratings

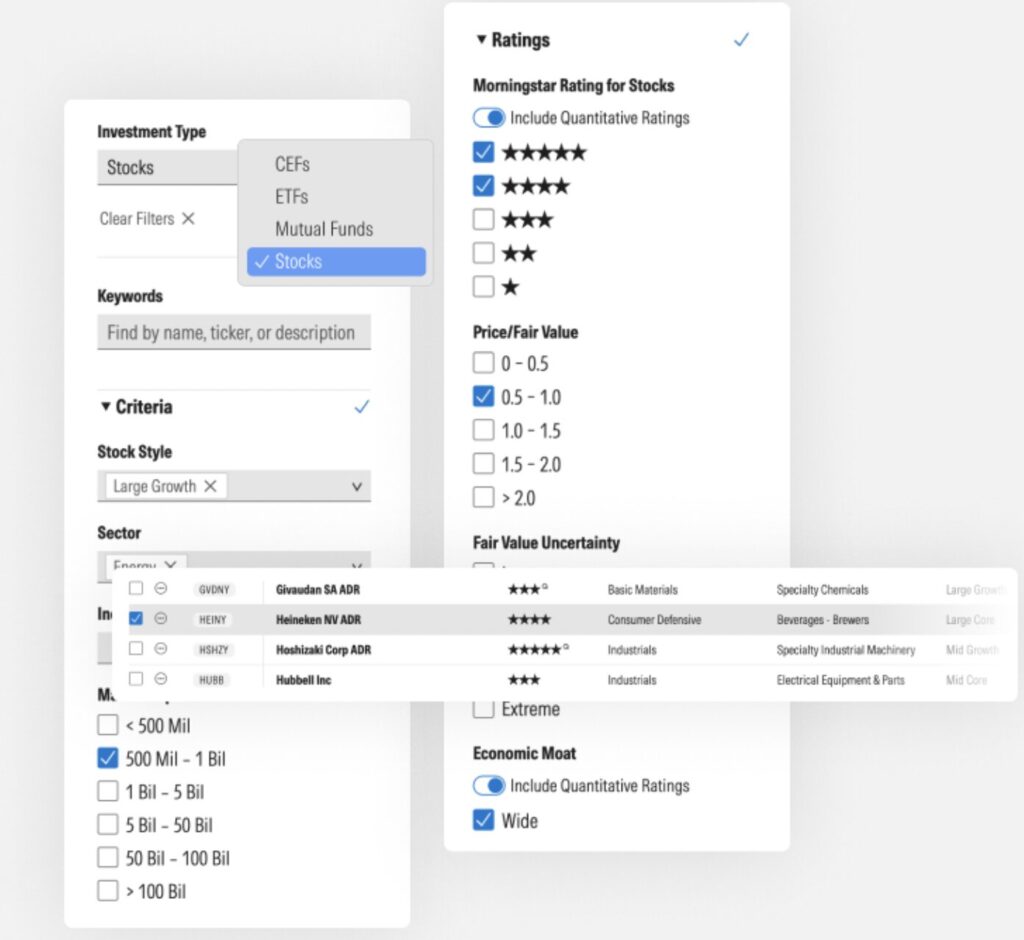

- Stock screener, fund screener, and ESG screener tools

- Portfolio X-Ray and portfolio monitoring tools

- Model portfolios and curated investment ideas

The scale is significant—Morningstar generates over $1.7 billion in annual revenue and maintains one of the largest independent equity research teams globally, with approximately 120 analysts covering around 1,000 equities in depth and detailed coverage of about 1,600 mutual funds across the US, Europe, and Asia.

You can access Morningstar Investor through the web platform or mobile apps on iOS and Android that sync watchlists and portfolios. That said, most serious work is still best done on desktop, where you can dig into the data-dense tables and multi-tab layouts.

Morningstar Investor Pricing in 2026: Is the Cost Justified?

At $249/year, Morningstar Investor costs about $20.75 per month when you do the math. Is that reasonable? It depends entirely on your portfolio size and how actively you’ll use the tools.

Current pricing options:

| Plan Type | Price | Notes |

| Annual subscription | $249/year | Standard rate, best value |

| Monthly subscription | $34.95/month | 41% more expensive than annual |

| First-year promo | ~$199/year | Typical discount after 7-day trial |

| Free trial | 7 days | Full access, cancel anytime before billing |

How the morningstar investor cost compares to portfolio sizes:

- On a $50,000 portfolio, $249 equals 0.5% per year

- On a $100,000 portfolio, it’s 0.25% per year

- On a $250,000 portfolio, it drops to just 0.1% per year

For investors with six-figure portfolios, the subscription cost becomes relatively trivial if it helps you avoid even one poorly performing fund or reduce expense ratios by 0.25%.

What’s free vs. what requires a paid subscription:

- Free: High-level fund pages, basic star ratings, limited articles, and snapshot data

- Paid: Full analyst reports, forward-looking Medalist Ratings, Portfolio X-Ray depth, advanced screeners, and custom watchlists with alerts

To use your 7-day free trial efficiently, follow this approach:

- Import or manually enter your actual portfolio holdings on day one

- Run Portfolio X-Ray to see your true asset allocation and any overlap

- Pull full analyst reports on your 3-5 largest holdings

- Build one custom screen based on criteria you care about (e.g., low-fee ETFs with 4+ stars)

- Set a calendar reminder for day 6 to make your cancel-or-keep decision

👉 If you’re curious whether Morningstar’s tools justify the $249 price for your portfolio size, you can test the full platform free for 7 days and run a complete Portfolio X-Ray on your holdings.

Core Features That Might Make Morningstar Worth It

The real value in Morningstar Investor isn’t flashy dashboards or gamified trading prompts. It’s the depth of fundamental research and diagnostic tools that help you understand what you actually own—and whether it’s serving your financial goals.

The platform’s key features fall into four main buckets: independent research reports, star and Medalist ratings, Portfolio X-Ray and portfolio management tools, and screeners with curated investment ideas.

This section walks through each, focusing on how they actually help you make better investment decisions rather than just listing menu options. Keep in mind that while these tools are powerful, they come with limitations—most notably a dated interface and the need for some manual data entry—which we’ll explore later.

Independent Investment Research & Analyst Reports

Morningstar employs around 150+ analysts globally who produce both qualitative and quantitative research on mutual funds, ETFs, and individual stocks. This is objective investment research in the truest sense—Morningstar doesn’t take trading commissions from investors and isn’t paid by fund companies to rate their products.

A typical fund or stock report includes:

- Strategy and investment process description

- Management tenure and track record

- Fee analysis comparing expense ratios to category peers

- Risk profile and volatility metrics

- Valuation estimates (for stocks) with long-term return expectations

- Sustainability ratings and carbon risk evaluations (for ESG-focused investors)

For example, a bond fund report might break down duration risk, credit quality distribution, and how fee drag compares to similar funds. A stock report on a wide-moat company like Microsoft might argue why it appears undervalued relative to Morningstar’s fair value estimate.

Only paying Morningstar Investor members get full access to these detailed analyst PDF reports and forward-looking commentary. Free users see partial snapshots—useful for curiosity, but not deep enough for serious investment decisions.

Morningstar Star Ratings & Medalist Ratings

Morningstar’s rating system actually consists of two separate systems, and understanding both is essential for getting value from the platform.

Star Ratings (1-5 stars): These are backward-looking ratings based primarily on risk-adjusted past performance over 3-, 5-, and 10-year periods versus category peers. Only the top 10% of funds in each category receive 5 stars. Importantly, costs are embedded in the methodology—high expense ratios drag down star ratings automatically.

Medalist Ratings (Gold/Silver/Bronze/Neutral/Negative): These are forward-looking ratings where analysts (and quantitative models) assess five pillars—process, people, parent company, performance, and price—to estimate whether a strategy can outperform its benchmark over a full market cycle.

The main criticism of Morningstar’s ratings is fair: they rely heavily on historical data and category definitions, which may limit predictive power. A 5-star fund today isn’t guaranteed to outperform tomorrow. Treat these ratings as a starting point for research, not a final decision tool.

Practical usage example: A DIY investor comparing two similar U.S. large-cap index funds might use Medalist Ratings to identify which has lower fees and a more sustainable investment process. Or they might use the ratings to flag a long-held active fund that’s now rated Neutral—prompting a closer look at whether past performance justifies continued ownership.

Portfolio X-Ray and Portfolio Monitoring Tools

Portfolio X-Ray is Morningstar’s signature diagnostic tool and arguably the feature that most justifies the subscription cost. It “looks through” your mutual funds and ETFs to expose the underlying holdings across your entire investment portfolio.

What X-Ray reveals:

- Exact stock and bond holdings aggregated across all your funds

- Sector and geographic breakdowns

- Style box exposure (large-cap value vs. small-cap growth, etc.)

- Fee drag across your portfolio

- Concentration in top positions

- Hidden overlap between funds

This matters because many investors don’t realize they own the same stocks multiple times across different funds. If you hold three different S&P 500 index funds plus a large-cap growth fund, you might have 40% of your portfolio in the same top 10 tech companies—creating unintended concentration risk.

The portfolio tracker component lets you connect brokerage accounts or enter holdings manually to view performance tracking, dividends, and rebalancing alerts. One caveat: performance data from linked accounts isn’t always perfectly automated, and manual transaction entry may be required for precise results.

The platform also includes watchlists and basic alerts for rating changes and major news affecting your holdings. Practically speaking, an investor could review their full asset allocation monthly in 10-15 minutes using these tools—checking for drift, overlap, and any rating downgrades.

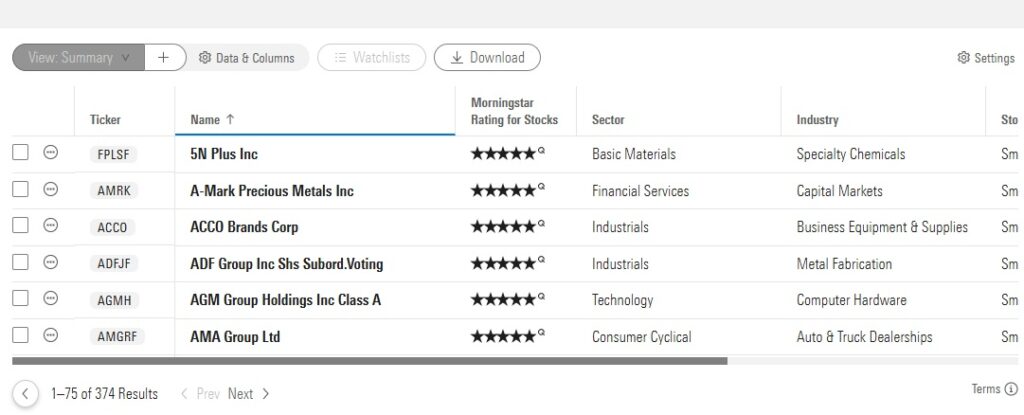

Screeners, Investing Ideas, and Other Tools

Morningstar offers stock, ETF, mutual fund, and ESG screeners that let you filter investments by dozens of data points:

- Expense ratios

- Performance metrics

- Star and Medalist ratings

- Sector and asset class

- Dividend yield

- Sustainability ratings

Basic screening is available free, but advanced filters and the ability to save custom screens require Morningstar Investor. For example, you might filter for U.S. value ETFs with expense ratios under 0.15%, at least 4 stars, and a Bronze or higher Medalist rating—narrowing thousands of options to a manageable list.

Investing Ideas and curated lists include:

- Analyst-selected “best ideas” for stocks and funds

- Model portfolios for different risk tolerance levels

- Themed lists (dividend growth, ESG leaders, low-cost index funds core holdings)

Additional tools include basic technical charts (though not as robust as dedicated trading platforms), comparison views across multiple funds, and educational resources like articles and webinars on diversification, risk management, and fee optimization.

While these tools are useful, they usually aren’t enough alone to justify the premium subscription. Their value is highest when combined with the research reports and X-Ray diagnostics to form a complete picture.

🔎 Want to see what your portfolio really looks like under the hood? Morningstar Investor’s Portfolio X-Ray tool lets you uncover hidden overlap, sector concentration, and fee drag in minutes. Try it free before committing.

User Experience: Strengths and Weak Spots

Morningstar prioritizes data density and research depth over sleek, modern design. The platform feels more like a professional database than a consumer fintech app—which is either a strength or weakness depending on your preferences.

The desktop web experience features data-rich pages full of tables, dropdowns, and multi-tab layouts. For experienced investors who want maximum information, this is powerful. For beginners, it can feel overwhelming. Pages load with substantial amounts of information, and knowing where to focus takes practice.

The mobile apps on iOS and Android essentially repackage the website experience. User complaints often mention horizontal scrolling requirements, smaller fonts, and less intuitive navigation compared to modern investing apps. If you’re used to Robinhood’s clean interface, Morningstar will feel dense.

One persistent frustration: even paying subscribers encounter in-page advertising and promotional banners, which some users find distracting given the premium service they’re paying for.

Tips for navigating the interface:

- Learn where key tabs live: Performance, Portfolio, and Ratings are your most-used sections

- Use the search function rather than trying to navigate through menus

- Bookmark your portfolio dashboard for quick access

Learning Curve and Complexity

Morningstar’s depth creates a genuine learning curve. New users may initially feel overwhelmed by terminology like “style box,” “upside/downside capture ratio,” “alpha,” and “tracking error.” This isn’t a platform designed for someone who’s never researched a mutual fund before.

A realistic onboarding path:

- Start by looking up funds you already own

- Read one full analyst report to understand the format

- Run X-Ray on your existing portfolio to see the diagnostic power

- Then explore advanced screeners once you’re comfortable

Morningstar offers glossaries, help articles, and some educational content, but these resources are scattered throughout the platform rather than presented as a cohesive learning journey. True beginners might find more beginner-friendly dashboards elsewhere, then graduate to Morningstar once they’re ready for deeper analysis.

Expect to spend a few hours “learning the system” during your trial week. Treat that time investment as part of evaluating whether you’ll actually use the service regularly.

Who Morningstar Is Best For (And Who Should Avoid It)

This is the decision-making core of any morningstar review. Here’s a direct breakdown of who should consider subscribing versus who should skip it.

Ideal Morningstar Investor users:

- Fundamental, long-term investors who research individual mutual funds and ETFs before buying

- DIY retirement savers with portfolios above $50,000 who want to optimize allocations

- Value-oriented stock pickers who read company reports regularly

- Investors holding multiple funds who need to check for overlap and hidden concentration

- Financial professionals managing client portfolios who need independent research

Who probably won’t benefit:

- Pure index investors holding only 1-3 broad market ETFs (you already know what you own)

- Hands-off robo-advisor clients who don’t make their own fund selections

- Day traders needing real-time quotes and advanced technical analysis

- Investors with very small portfolios where the $249 cost represents a significant percentage

Brief personas:

- 45-year-old 401(k) investor rethinking a complex mix of active funds accumulated over 20 years → Morningstar is likely worth it for fund analysis and overlap detection

- 25-year-old who auto-invests $500/month into a single total-market ETF → Morningstar is probably overkill

Before subscribing, honestly assess your behavior: Will you realistically log in at least once a month to run X-Rays, read analyst reports, or adjust your strategy? If not, the subscription won’t deliver enough value.

Portfolio Size and Engagement Level

Portfolio size directly affects whether the morningstar investor worth proposition makes sense mathematically.

Portfolio size thresholds:

| Portfolio Size | $249 as % of Portfolio | Verdict |

| Under $10,000 | 2.5%+ | Hard to justify |

| $10,000-$20,000 | 1.25-2.5% | Usually not worth it |

| $20,000-$50,000 | 0.5-1.25% | Worth it if actively engaged |

| $50,000-$100,000 | 0.25-0.5% | Often worth it for many investors |

| $100,000+ | Under 0.25% | Generally worth it for engaged investors |

Beyond size, engagement level matters enormously. Morningstar delivers the most value to investors who actively research, rebalance at least annually, and adjust fund lineups based on new information—not those who set an allocation once and ignore it for years.

Think about it this way: If Morningstar helps you identify and replace even one fund with unnecessarily high expense ratios (saving 0.25%-0.50% per year), or avoid a chronic underperformer, the subscription pays for itself on portfolios above $50,000.

One important note: Many large brokerages and public libraries provide free access to some Morningstar reports. For investors with modest portfolios, checking whether your broker or library card grants access might be “good enough” without paying $249 directly.

Pros and Cons: Morningstar’s Real-World Trade-Offs

No investment tool is perfect. Here’s a balanced view of what Morningstar does well and where it falls short.

Pros:

- Independent research without conflicts from trading commissions or fund company payments

- Unmatched depth of mutual fund and ETF coverage (1,600+ funds with detailed analysis)

- Portfolio X-Ray reveals hidden overlaps and concentration risks that other tools miss

- Over 30 years of credibility behind the star rating system and Medalist methodology

- Institutional-grade data and analyst reports accessible to individual investors

- Sustainability ratings for ESG-focused portfolio builders

Cons:

- Relatively expensive at $249/year compared to free brokerage tools

- Dated interface that feels clunky compared to modern fintech apps

- Manual data entry often required for accurate portfolio tracking and performance tracking

- Heavy reliance on past performance data, which may limit future performance predictions

- Some negative reviews cite mixed customer service experiences

- In-page advertising appears even for paying subscribers

One specific practical con worth noting: Performance tracking from linked brokerage accounts isn’t always fully automated. If you want precise portfolio’s performance data, you may need to manually enter transactions—a time investment that casual users might not make.

How to Test Whether Morningstar Is Worth It for You

The best way to decide is to use the 7-day free trial as a structured experiment rather than casually browsing around.

Your trial week action plan:

- Day 1: Import or enter all your existing investment accounts and holdings

- Day 2: Run a full Portfolio X-Ray to see your true asset allocation, sector exposure, and any fund overlap

- Day 3-4: Read detailed analyst reports for your top 5 holdings—note any surprises or concerns

- Day 5: Create 1-2 custom screens based on criteria relevant to your strategy (e.g., low-cost dividend ETFs)

- Day 6: Set your calendar reminder and make your decision

Questions to answer during your trial:

- Did X-Ray reveal overlapping funds or unnecessary concentration you weren’t aware of?

- Did any analyst reports change your view on a current holding?

- Did you discover potential investments that fit your criteria better than what you own?

- Will you realistically repeat this research process several times per year?

Quantify potential value: If you identify even one expensive, underperforming fund you might replace, estimate the annual fee savings. On a $50,000 position, replacing a fund with 0.75% expense ratio with one charging 0.15% saves $300/year—more than the subscription cost.

If you don’t learn anything new or don’t feel motivated to log in after the first few days, cancel before the trial converts to a paid subscription. There’s no shame in relying on freely available information if Morningstar’s depth isn’t delivering insights you’ll act on.

Bottom Line: Is Morningstar Worth It in 2026?

Morningstar Investor is worth the $249 annual cost for a specific type of investor: serious, fundamentally oriented, long-term investors with meaningful portfolios who are willing to engage with detailed data regularly. If that description fits you, the platform’s independent research, comprehensive fund coverage, and portfolio diagnostic tools can genuinely improve your investment decisions and potentially save you far more than the subscription costs.

The key conditions that make Morningstar worth paying for:

- Portfolio size above $50,000 (making the fee a small percentage)

- Genuine interest in reading analyst reports and understanding fund analysis

- Complex holdings across multiple mutual funds and ETFs where overlap and risk management matter

- Willingness to log in at least monthly to review allocations and ratings changes

Conversely, Morningstar probably isn’t worth it if you have small balances, maintain an ultra-simple index-only portfolio, pursue day-trading strategies, or aren’t willing to climb a learning curve. For these investors, free tools from brokerages or library access to Morningstar reports may suffice.

Think of Morningstar Investor as a powerful decision-support and risk-diagnostic tool—not a shortcut to “hot tips” or guaranteed outperformance. The platform excels at helping you understand what you own, why you own it, and whether it still makes sense for your financial goals.

If you’re still undecided, here’s your practical next step: Run a one-time Portfolio X-Ray through the free trial (or via broker access or your local library) to see your current portfolio’s true shape. That single diagnostic often reveals enough insights to make your subscription decision clear.

📊 If you’re a serious, long-term investor actively reviewing your holdings, Morningstar Investor is worth testing. Start with the free trial, run your analysis, and decide based on real data — not guesswork.

FAQs

Morningstar is usually not worth it for complete beginners. The platform is data-dense and designed for investors who already understand mutual funds, ETFs, valuation metrics, and asset allocation. New investors may find free brokerage tools or simpler platforms easier to navigate before upgrading to Morningstar Investor.

If you hold just one or two broad market index ETFs and rarely rebalance, Morningstar is probably not worth the $249 annual fee. You already know your exposure. However, if you own multiple funds and want to analyze overlap, sector concentration, and hidden risk, Portfolio X-Ray may justify the cost.

Morningstar’s Star Ratings are backward-looking and based on risk-adjusted past performance, while Medalist Ratings are forward-looking assessments from analysts and quantitative models. They are useful research tools, but no rating system guarantees future performance. They should be used as a starting point—not a final decision.

Morningstar typically provides deeper mutual fund analysis and more comprehensive ETF coverage than most brokerage platforms. Free brokerage research is often sufficient for stock investors, but fund-focused investors may find Morningstar’s reports and Portfolio X-Ray tools more detailed and independent.

Yes, Morningstar Investor offers a 7-day free trial. This allows full access to analyst reports, Portfolio X-Ray, screeners, and ratings. Using the trial to analyze your existing portfolio is the best way to determine if Morningstar is worth it for your situation.